Blitzscaling Insurance with Acko

With an expected valuation >$400M in 2.5 years of trading, Acko is a rocketship! Here's some insights into the business that's about to raise a $60M Series D.

Upon hearing that Munich Re Ventures is rumoured to be investing $60M-$70M into Acko Insurance at a valuation between $400M to $500M [1], I couldn’t control my excitement - I’ve been following Acko since its $12M Series B funding from Amazon [2] in 2018.

This write-up is split into two parts:

The high-level overview

Company growth data

Introduction

Acko is a licensed insurance company in India; founded by Varun Dua (who co-founded Coverfox - an insurance web aggregator). It raised a $65M Series C round in March 2019 [3].

From an outsiders view, Acko focuses on B2B2C insurance sales (“embedded insurance”) via its partners such as Ola Cabs, RedBus etc. Contrary to popular perception, it has a strong D2C distribution play as well (if you’re in India, you’d bear witness to their performance marketing campaigns!)

What is Acko famous for?

Acko underwrites ~ 20M micro-trip policies per month via its partnership with Ola Cabs [4]

Acko x Amazon - Acko has been supporting Amazon in its insurance distribution foray via Amazon Pay [5] It is no secret that payment platforms in India are keen to enter insurance [6]

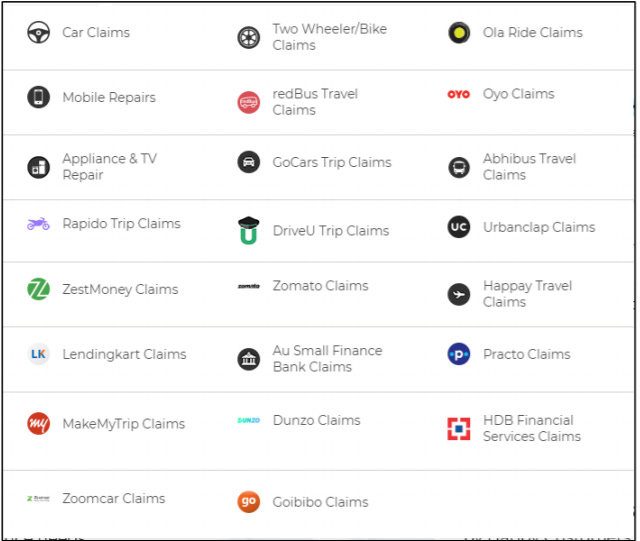

To highlight how many “channel partners” Acko works with, it’s best to see the screenshot from their website below:

If you haven’t heard of Acko, the above section should provide some “high-level” information. Next, let’s look at their (astounding) growth figures.

Acko’s growth - Gross Premiums

It is fair to interpret Gross Premiums as a top-line revenue metric i.e. since it began selling policies in November 2017, Acko has reached ~ $4.4M in monthly revenue.

For FY 19-20, Acko’s revenue was ~ $55.44M; which is very impressive for a company that has been trading for just under 2.5 years!

Acko’s growth - team size

Looking at team size as a metric for future growth is a questionable approach for software businesses. However, for an insurance company, there are significant economies of scale w.r.t workforce over time.

Data from LinkedIn highlights they’ve got 91 engineers (i.e. ~ 20% of their team) which is their single biggest functional unit.

Regulatory filings corner

If you’re not keen to jump into this section, please feel free to skip it! Please note - audited financial statements for the quarter ended March ‘20 are not available as yet.

First, let’s look at some key insurance metrics:

If none of these make sense to you - don’t worry! The KPI for insurance is the Combined Ratio (i.e. claims payouts + loaded expenses expressed as a % of premiums collected) - below 100% would be ideal.

The Initial Loss Ratio (i.e. initial claims payout as a % of premiums collected) is more of a guide for pricing (or “attritional” i.e. high-volume, low cost claims)

Acko’s combined ratio of 214% but initial loss ratio of 59% is driven by two factors:

Nature of motor insurance loss development - Motor insurance claims take time to “fully evolve” (legal battles & expenses are long drawn); as we’ll see shortly - Acko‘s business is significantly driven by motor insurance.

Acko is still “early stage” - It’s high combined ratio is indicative of high management expenses (which are expected in the early days of an insurance company).

Next, let’s look at Acko’s “business mix” i.e. the composition of its revenue.

From a top-line revenue perspective, Acko is slightly “over-exposed” to motor insurance (composed of Own Damage - OD and Third Party - TP) with ~ 55% of its top-line coming from this category. For benchmarking purposes, the industry average for motor insurance contribution is ~ 47.5%.

Finally, let’s examine the split between “embedded” insurance and D2C (direct-to-consumer) business:

From the above, we see that whilst D2C accounts for only 55% of policies sold - it accounts for 81.15% of Acko’s revenue i.e. D2C policies tend to be of a higher average sum assured (and, therefore premium) as compared to the B2B2C policies.

This shouldn’t come as a surprise given the earlier reference to Acko’s partnership with mobility providers such as Ola, RedBus etc - these are volumes plays! If nothing else - we know the data confirms the press releases!

There’s much more to dissect in the regulatory filings but I think this should give you a flavour - if you’d like to find out more details; feel free to drop a comment.

Blitzscaling takes its toll

“If It Doesn't Hurt You're Not Doing It Right” - Practically Single

To make this a balanced piece on Acko, it is important that I highlight that blitzscaling isn’t easy. Even the best of us face trouble -

Acko was fined a total of ~ $135,000 in January 2020 for four different actions including potentially misleading advertisement on motor insurance and not properly disclosing their advertisement campaign with Amazon [7]

Acko has run into a legal suit with two of its ex-employees around IP theft in May 2020 [8]

Final thoughts

Personally, Acko is doing a fantastic job. At a lower-end of the valuation spectrum in the upcoming round, Acko would be valued at 7x trailing annual gross premiums (i.e. top-line revenue).

Whilst an embedded value approach would be more informative on rationalizing price, it is a tedious task - if you’re keen to go down that route, feel free to ping me!

Hopefully you find this read on Acko to be informative/interesting. If it was, please do leave a comment below and/or share this with everyone else!

It was intellectual insights..Thanks..

Thanks for covering Acko. It's fantastic :)