Unboxing the IRDAI InsurTech sandbox

Unboxing the IRDAI InsurTech sandbox

67 approvals over a 6 month period: "on-demand" motor insurance, wearable-linked health insurance & more - the IRDAI is firing on all cylinders.

Regulatory sandbox schemes have become a recurrent phenomenon (especially in the context of FinTech). In brief, these sandbox schemes (supported by the concerned regulator) allow start-ups and incumbents to “alpha launch” new products or services to a limited number of (volunteering) customers.

This brief mailer will provide some global context to the IRDA InsurTech sandbox (India) along with international parallels to pilots taking place in this sandbox.

For InsurTech startups, there are several sandbox schemes globally (listed in order of starting date for Cohort I):

FCA Regulatory Sandbox (UK) - launched in 2016

MAS FinTech Sandbox (Singapore) - launched in 2016

BMA Sandbox (Bermuda) - launched in 2018

GFIN (Worldwide; 17 countries) - launched 2019

IRDAI InsurTech Sandbox (India) - launched 2020

SECP Regulatory Sandbox (Pakistan) - launched 2020

If you’ve got specific questions about any of the above, do let me know! For now, let’s dive into the IRDAI InsurTech sandbox

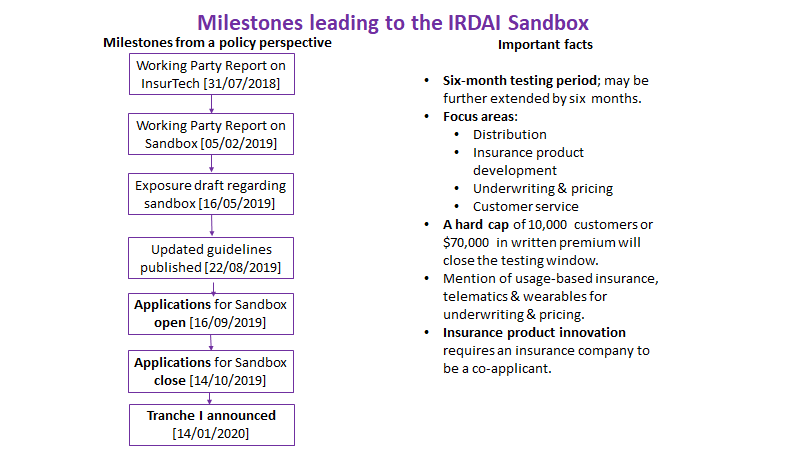

Policy and related milestones

The IRDAI (India’s insurance regulator) first acknowledged “InsurTech” in July 2018 - deeply etched in my memory since I wrote my 1st ever article on their InsurTech report [1].

To be honest, I don’t want to bore you with the milestones (below) but I want to highlight the “sandbox constraints” (after the info-graphic)

Constraints imposed by the sandbox:

Each pilot takes place over a 6-month testing period (extendable by a further 6 months)

The pilot “closes” at the earlier of 10,000 customers serviced or ₹50,00,000 ($70,000) in Sum Assured (i.e. insured value) written.

Any InsurTech start-up wishing to sell an insurance policy through the sandbox must have the policies “underwritten” (i.e. backed) by an insurance company in India. *

* A common criticism of sandbox schemes is the lack of a dedicated pool of “insurance capacity” for start-ups to experiment with novel products. I’ve personally witnessed founders taking 40+ meetings & 6+ months to find an incumbent insurer to join them in a sandbox. i.e. a sandbox isn’t a complete solution but a step in the right direction.

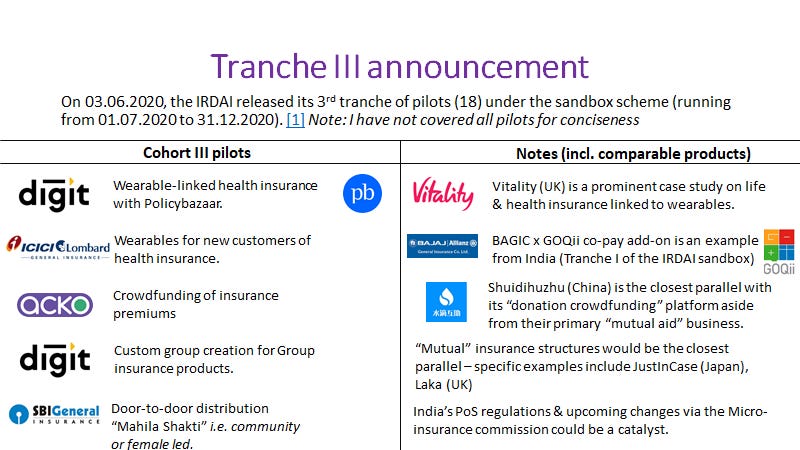

Recent announcement - Tranche III of the sandbox

Whilst most sandboxes have at most 20 pilots running concurrently, in July 2020, the IRDAI sandbox could be running 67 pilots concurrently.

On 03.06, Tranche III was announced [1] (info-graphic below) and some of the pilots caught my eyes.

More wearable-linked health insurance:

Digit and Policybazaar is an interesting combination (neo-insurer x India’s largest price comparison website) - though I’m not sure who their hardware partner is!

As a side-note, approvals were granted for similar products in Tranche I too! GOQii is the partner for Bajaj Allianz & Kotak Mahindra’s respective wearables-linked health insurance pilots. [2] [3]

Another side note, these pilots aren’t using wearables data to calculate premiums based on individual health risks. However, they’re adopting a similar model to Vitality by “nudging” good behavior via rewards including renewals premium discounts or co-pay (proportion of health claim borne by you to align incentives) adjustments.

Digit’s custom group product (health)

A “group” product is typically sold to an employer or “scheme” manager (e.g. co-operative, membership association). To avoid adverse selection (i.e. only unhealthy folks piling in), “group” products in an employer context must include every eligible employee (eligibility might be on the basis of employment status or age).

Effectively, Digit is breaking with convention here and allowing a group of individuals to come together and “negotiate” a group health insurance cover (typically better rates + wider coverage scope)

I can’t think of an international comparable - the closest would be the “mutual” (i.e. risk pooling) structure of Laka and JustInCase but it would be a weak comparison at best.

Acko’s crowdfunding of premiums

Sounds exciting but I couldn’t decipher this - I somehow recall Shuidihuzhu’s donation crowdfunding feature i.e. if an individual’s insurance cover via the platform doesn’t meet all hospitalization/medical expenses, other users can “donate”.

This could just be that donation crowdfunding feature but applied to premium payments rather than medical reimbursements.

Tranche III seems promising!

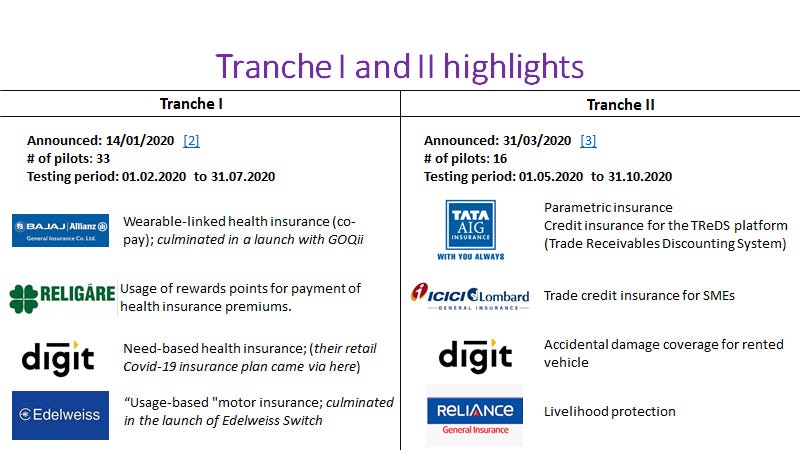

Tranche I and Tranche II

Below is an info-graphic on key pilots from Tranche I and Tranche II [4] [5] :

As you’d expect - I couldn’t possibly cover 49 pilots within this write-up but some pilots you should take note of are:

Digit’s “need-based health insurance”

Digit was the 1st company to roll-out a Covid-19 specific health insurance product in India in early March! This was possible under the “need-based” insurance product regime of this sandbox.

Whilst the benefits of a standalone Covid-19 health insurance product are debatable [6], it was fascinating to see insurance companies launch a new product within days!

The Covid-19 insurance product arms race in India demonstrates that a combination of regulatory support (sandbox “need based” products) and industry initiative can turbocharge product innovation.

Tata AIG’s parametric insurance

Think of parametric insurance as an “if-else-then” statement i.e. if a pre-defined event occurs (the “trigger”) ; then a claims payout follows automatically.

Parametric insurance is touted as the next “big thing” due to climate change - some start-ups you should check out in this space are FloodFlash (flood insurance; UK); Wetterheld (crop damage insurance; Germany) and Blink (travel insurance; worldwide)

Parametric insurance (together with index and weather-linked “triggers”) could revolutionize agricultural insurance in India and speed up disaster response (recall, India stack i.e. Aadhaar & UPI provide pre-built rails for large scale funds disbursal).

ICICI Lombard’s trade credit insurance

Several corporate & SME transactions take place on “credit” (i.e. the buyer is extended a payment window/payment schedule by the seller). This implies that the seller is exposed to a “credit event” (i.e. buyer goes bankrupt)

Note: Bills Receivable discounting refers to a “loan”or “advance” given by a bank to a seller to meet working capital requirements. The “collateral” or security offered by the seller is “a promise to pay” from one of its buyers.

Bills Receivable discounting only solves for the “short term financing crunch” for an SME - a complete solution would require trade credit insurance i.e. an “insurance policy” against the default of a buyer”.

Don’t be surprised if every SME platform (e.g. Khatabook, BharatPe, PhonePe etc) bundles trade credit insurance & Bills Receivable discounting into a single fee; early signs found in TATA AIG’s offering for the TReDS platform of the Receivables Exchange of India.

That’s all for the IRDA Sandbox; next to some concluding thoughts

“Regulation as an enabler”

The Indian insurance industry is conservative to say the least. Most carriers adopt a “wait to hear regulator’s viewpoint” approach since the “status quo” produces 15% YoY growth.

In such a marketplace, innovation is an after-thought but the swift launch of Covid-19 insurance products via the sandbox instills some hope in me.

To maintain a balanced viewpoint - the current “on-demand” motor insurance products in India are a far cry from what some Western peers offer (topic for next week) & similarly for wearable-linked health insurance. However, India has a tendency to leapfrog (platforms, and therefore products) - don’t lose faith!

If you found this summary of the IRDAI InsurTech sandbox interesting- do leave a like below! Also, do share this with teams at platform economy start-ups who might be curious as to the “Who, What & Why” of partnering with insurance companies - I’m happy to take any questions on Twitter (including DMs).

Hi Rahul, one quick question here, what do you see as the main reason for limited entries from life insurance players vis a vis non life and health in the entire list of 67 approved entities, is it the complexity of products or longer contract tenure as the main bottleneck for not too many takers for this sandbox environment.

Thanks