Insurance as a feature; not a product

An overview of "alternative" (i.e. digital) distribution of insurance products by FinTech apps, e-commerce marketplaces and verticalised marketplaces in India..

Hi folks! This post deviates from the normal.

I’m won’t be commenting on InsurTech fundraising, partnerships or press releases. I’ve been following platform & FinTech led distribution of insurance (“cross-selling” or “value-add”) for a while and feel the need to share an observation I’ve made -

In India, increasingly insurance is becoming a feature, not a product

This observation (and post) was initially sparked by a Tweet from Kunal Shah, Founder of CRED & Freecharge (sold for $450M), which I’ve provided below:

If you’re looking for the TLDR; just replace “lending” with “insurance” above.

First, “insurance as a feature; not as a product” is nothing new.

The concept of an “affinity channel” (i.e. distribution channel owned by a partner) is well accepted in insurance

Insurance is traditionally an intermediated business; either via brokers or banks/financial institutions or membership associations. Therefore,the concept of paying “commissions” to distribution partners is well entrenched in insurance.

However, the emergence of platform economies presents a new “affinity channel”

When viewed from the lens of an insurance company, partnering with CarDekho is (pretty much) the usual car dealership partnership for insurance sales (albeit some elements of O2O2O i.e. online-to-offline-online).

However, viewing this from CarDekho’s lens, insurance is a “feature” in their overall “one stop shop for (used) car purchase” customer value proposition.

In short, perception matters - “new affinity channel” for insurers but “insurance is a feature; not a product” for platforms.

To support my observation, I’ll provide you with examples from:

Payments focused FinTechs

E-commerce marketplaces

Verticalised marketplaces

Note: My goal isn’t to provide a strategy deep-dive but rather is to have this write-up act like a “book-mark” of sorts for you to refer back to from time to time!

Let’s begin with MobiKwik in the Payments focused FinTechs segment:

MobiKwik

Although Paytm was the “1st mover” into insurance; MobiKwik is a front-runner when you look at the number of insurance products it has offered its customers -

If you notice carefully, there is a lot of life insurance distribution above (unique to MobiKwik). But, MobiKwik doesn’t stop there - it recently began its foray into health insurance via a cancer insurance product & Digit’s Covid-19 insurance product:

Closely following MobiKwik in terms of insurance related activity is Paytm

Paytm

Arguably, Paytm forayed India’s 1st super-app play; from mobile recharge & payments, it now offers Mutual Funds, gold purchases, “mini-programs” (oddly reminiscent of WeChat) and insurance too!

Do note that Paytm has an insurance brokerage licence (MobiKwik & PhonePe are “corporate agents” which caps the number of insurers they can work with)

More recently, Paytm offered Reliance General Insurance’s Covid-19 insurance product (which is by-far the most comprehensive out there by including Loss of job cover and Loss of Income cover)

Paytm’s insurance foray shouldn’t surprise you in light of their super-app strategy (as a side note - Paytm’s mini-program ecosystem & insurance brokerage reminds me of Tencent owned WeChat’s mini-program ecosystem which hosts WeSure - Tencent’s insurance distribution arm).

Next, to PhonePe!

PhonePe

With its origins linked to UPI and the unsolved need for a “QR code aggregator”, PhonePe has had to rapidly evolve from a UPI-first payments platform as UPI fees get squeezed.

PhonePe is the latest entrant into insurance distribution game with a travel insurance product (bad timing!) and Covid-19 insurance product.

Props to PhonePe; BharatPe too launched health insurance recently.

I’ve personally not seen a lot in the Payments Bank space apart from Airtel Payments Bank (arguably Jio Payments Bank might be interesting; I wrote about that earlier)

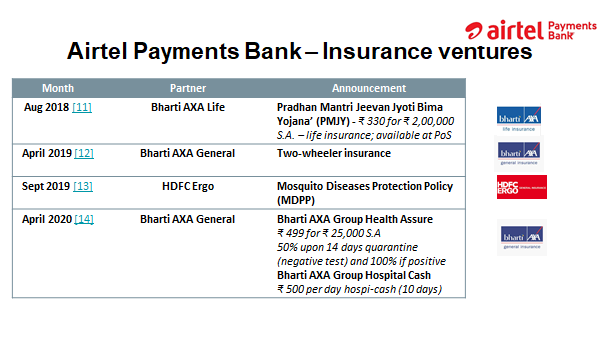

Airtel Payments Bank

The Telco x Insurance model is very well established for emerging markets (pioneered in Africa). Therefore, Airtel Payments Bank working to distribute insurance products isn’t surprising and more so since it is selling products underwritten by Bharati AXA (Life & General) - it makes sense to have companies within a single group partner together!

Okay, enough FinTech stuff - next to e-commerce marketplaces.

Amazon

With an equity stake in Bankbazaar and Acko, Amazon seems to be very bullish on finance in India (likewise in the USA where Haven Life - their employee benefits Joint Venture with Berkshire and JP Morgan makes people suspect the “AWS for Healthcare” is here!).

Amazon hasn’t made any major moves in insurance as yet; though, I suspect Amazon Pay will eventually get a web aggregator licence (like Policybazaar) to capitalize on the organic traffic that Amazon pulls. Watch out!

I’ve got an extended thesis on Big Tech x Insurance which I’ll publish someday. For now, let’s look at India’s Amazon - Flipkart.

Flipkart

I love Flipkart’s approach of using its vast distributor network as a platform to sell insurance; I personally believe that several other marketplace start-ups will follow suit.

Okay, enough e-commerce marketplace - let’s move to verticalised marketplaces (I’m only going to talk about motor marketplaces using CarDekho as an example)

CarDekho

As a car marketplace, you might believe (after scrolling through the above) that CarDekho is big on motor insurance; well that’s the tip of the iceberg - their subsidiary InsuranceDekho had sold 800,000 policies (across life, health & motor) in under one year!

At this point, I might be getting repetitive so I’ll close my “evidence” section by pointing out that you should expect Cars24, Droom and CarTrade (CarDekho’s competitors) will enter insurance too!

Perhaps, at this point, you’re convinced that insurance is indeed a “feature” similar to Kunal’s assertion for lending.

Closing thoughts

This concept of insurance as a feature is closely linked to “embedded insurance”, suggested by industry insiders like Nigel Walsh. Whilst there is a strong economic argument (“Economies of Scope” i.e. increase CLTV on sunk CAC), embedded insurance is fraught with mis-selling. A major case was PPI in UK [a] and in India - Maruti & Hero Insurance brokers [b] Professor Manoj Kumar highlighted the lack of customer awareness w.r.t insurance “bundled” into purchases.

Hence, my request to product teams is to default “opt out” of bundled insurance at purchase windows. As for standalone insurance purchases on digital platforms, I’ve seen clear & concise communication of policy wordings - which is great!

I intend to write a Part II covering the underlying strategy, common pitfalls and international case studies on “insurance as a feature”; if you’re keen to collaborate or share data/insights from your platform, do ping me!

To close out, if you found this useful - please feel free to like, subscribe or comment. Additionally, if you’re working on a platform and you’re looking to offer insurance to your customers, do get in touch with me - I’d love to hear more.

Sounds like Cake to me!

This was a very detailed and insightful read, considering there are very few articles about affinity insurance in India.

Can you suggest some other material where I can find more about these affinity insurance products?

Keep up the good work. All the best. 👍🏻