A comprehensive approach to pandemic risk management

Introduction

At the time of writing, Covid-19 has been declared a pandemic event by the WHO [1] with 1.275M reported cases and 69,500 deaths [2]The objective of this piece is to answer the following question – “How do we better prepare for a future pandemic?” The answer lies in public-private partnership, development bonds and insurance products.

“Life insurers and other businesses hold pandemic risk on their books already, but the risk is not being properly mitigated.” National Academy of Science [i]

Before we begin, it is fair to acknowledge existing pandemic risk transfer instruments:

(a) Swiss Re Corporate Solutions [3]

Their non-physical damage business interruption product provides an appropriate level of coverage.

(b) PathogenRX by Munich Re and Metabiota (also distributed by Marsh) [4]

A dedicated pandemic risk product

(c) African Risk Capacity [5]

Their O&E (Outbreaks & Epidemics) product is likely to provide relief against Covid-19 [6]

(d) World Bank Pandemic Emergency Financing [7]

This outstanding bond is like to produce outstandingly negative results for investors.

Product design framework recommendation

Steve Evans, rightly pointed out that the focus should remain on Product Design[8] i.e.

(a) Trigger definition

(b) Premium payment structure

(c) Go-To-Market (i.e. distribution channel)

As a statistician by training, I can vouch for the fact that insurance is more than an educated gamble – the US gambling industry is worth $240bn per year [9] – I agree with Steve, there is more than enough money floating around to “gamble” with.

I propose a Public-Private Partnership to create a dedicated facility (similar to the African Risk Capacity) for comprehensive pandemic (and epidemic) risk ex-ante mitigation, parametric transfer and on-set management capability.

There’s a lot to unpack in my product design recommendation above; in subsequent sections, I will answer why we should look to:

(a) Public-Private partnership

(b) Parametric transfer

(c) Ex-ante mitigation

(d) On-set management capability

Why now?

“Rahul, Covid-19 has already struck. What’s the point of looking at a capital markets solution for pandemic risk; we’ve already faced the event.”

i. Perhaps you’re right in the short term but, you’ve fallen victim to the Gambler’s Fallacy[10] – the recent occurrence of Covid-19 does not imply that another pandemic event won’t happen anytime soon.

ii. In fact, as described by Munich Re below [11] , it is likely that the next major epidemic or pandemic might around the corner (notice how the inter-event “waiting time” is compressing as we move forward in the timeline!)

iii. Furthermore, if you’ve worked in insurance, you’ve probably heard people defer the purchase of insurance by stating “that won’t happen to me!” Well, it just did and you better prepare for what’s to come next.

Several folks have pointed out, rather morbidly, that just as life insurance purchases are trigger by major life events (e.g. marriage, family death, mortgage etc), interest in pandemic risk management will remain sky-high for the forseeable future (institutional memory runs short, human memories stay for a lifetime). It seems that interest in Munich Re’s PathogenRX product has remained high since January ’20[12]

Hopefully, you’re convinced that this is the right time to explore a pandemic risk management facility. My arguments lie in the Gamblers Fallacy, shorter inter-outbreak waiting times and public “scar-tissue”.

Public-Private Partnership

Having donors pay insurance premiums obscures the useful link between the price of the premium and the strength of the preparedness system. – National Academy of Science[i]

Skin-in-the-game for ultimate cedants of risk (i.e. you, I and a 30-person SME) is absolutely critical for successful parametric risk management.

Please note: I’ll return to the link between premium and the “preparedness” system shortly, For now, let’s focus on the “donor aspect.”

Here is a comment from Nature[ii] on the “failure” of the World Bank Pandemic Emergency Financing (PEF) bond:

“Fanfare around the PEF might have encouraged complacency that actually increased pandemic risk. Following false assurance that the World Bank had a solution, resources and attention could shift elsewhere.”

Pay specific attention to the above observation; 3rd party assurance creates misaligned incentives (part of the reason why co-pay exists on health insurance products) – by forcing private market entities to share the premium “burden” with sovereigns, it creates mutual skin-in-the-game to develop disaster response and recovery mechanisms.

PRODUCT DESIGN: PREMIUM PAYMENT STRUCTURE

I propose that the insurance premiums are jointly borne by:

(a) Federal governments

· Preferably, bi-lateral or multi-lateral since prompt disbursal of funds can help contain pandemic risks within a given geography (there is a strong positive externality for adjacent countries when risk is contained within a country. [i])

(b) Private institutions (via dedicated levies or taxes)

· For example, UNITAID, focused on countering HIV, acquires 60% of its overall funding from a levy on airline tickets [i]).

· There is an argument that such levies might fall upon deaf ears thereby defeating the purpose of private partnership.

· Alternatively, an explicit levy similar to FloodRe (UK) on UK homeowner’s insurance policies could be used to amass private funds [13]

(c) Donors (especially for lower income countries)

· The IFFIM (Intl Finance Facility for Immunization) is a vehicle that pools pledges from multiple developed economies to offer finance for immunization. [14] A similar structure could be explored for pandemic risks too!

Realistically, I don’t expect option (c) to materialize in the near future and (a) might pose some political challenges. Maybe, sticking to private markets i.e. option (b) might be a more tangible immediate solution.

Parametric risk transfer

The idea of parametric risk transfer is predicated on the “If-else” statement in computer programming i.e. “If [event occurs] then [perform some action] else [perform some other action]”. In reality, a parametric insurance contract would have a “trigger” event (to release funds) that has several nuances to it such as:

(a) Staggered trigger (i.e. several layers to trigger)

(b) Trigger pre-requisites (corporate finance folks can view this as bond covenants)

In an epidemic, more than in almost any other situation, the dollar’s present value far exceeds its future one.” - National Academy of Science [i]

The importance of timely intervention is highlighted by the African Risk Capacity (ARC) where each $1 released via their parametric product is equivalent to $4.4 spent via traditional appeal/indemnity solutions. [15]

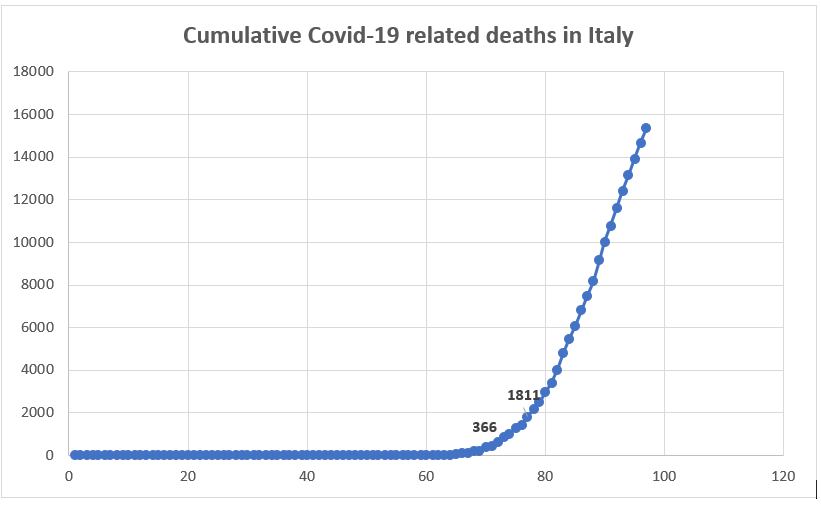

If you still remain unconvinced, hopefully, the situation in Italy might change your viewpoint.

Using data from ECDC on 05/04 [iii], you can see that if the World Bank’s PEF trigger was indeed 250 deaths [iv]with an (over) optimistic 1 week lag between fund release and funds disbursal, deaths would have increase over 5x to 1811 from 366.

Therefore, it is of paramount importance that a parametric product be used versus an indemnity product which would require loss adjustment. Every day counts.

With the correct infrastructure in place, a parametric insurance product can provide immediate relief (via direct benefits transfer) to citizens who are identified to be at-risk (i.e. daily wagers, elderly etc). The correct infrastructure is in place in:

(a) India with the Unified Payments Interface, Aadhaar card and Jan Dhan Yojna bank accounts (i.e. payments rails, identification and bank accounts)

(b) Kenya due to the presence of M-Pesa

For perspective, you can refer to the Direct Benefits Transfer success in India for LPG (Liquified Petroleum Gas) [16]

Trigger pre-requisites

Broadly, the pre-requisites allow for premium payments to be tied to strength of the preparedness system. You can split pre-requisites into pre-event and onset phases.

The objective is to minimize total economic and human loss especially in Low Income Countries (LIC). The image below from NCBI [v] highlights the most cost-effective solutions for saving lives in a pandemic event in LICs.

PRODUCT DESIGN: PRE-EVENT TRIGGER PRE-REQUISITES

To encourage pandemic response readiness for cedants, I would suggest the following pre-requisites for the trigger to be activated:

Demonstration and subsequent audit, on a bi-annual basis, of:

(a) Public sanitation infrastructure *

· Livestock management (to curb spark risk)

· Urban centres (to curb spread risk)

(b) Government stockpile of PPE (personal protective equipment) and basic sanitation equipment for frontline workers (e.g. law enforcement, essential infrastructure staff etc) *

(c) Government stockpile of essential goods (primarily food grains) and a distribution mechanism.

(d) Contact tracing & limited surveillance mechanisms**

· GOQii – India (15/03) [a]

· AliPay Health Score – [b]

* We’ll return to funding for infrastructure in a subsequent section

**To allay privacy concerns, these mechanisms can be instituted on-demand rather than continuously; GOQii took a week to launch the same; hence, PPP is essential to leverage the private sector’s speed to market

The role of technology is paramount for the above pre-event risk management

- A combination of geo-coded video assessment, purchase invoices and storage receipts can be used to verify Government stockpiles of necessary equipment and necessities.

- Contract tracing tools can be easily tested remotely via a code audit or limited field trial.

Let’s now assume that a pandemic event has occurred and the 1st tranche has been paid out. How do we continue to create an incentive structure to ensure that investors are satisfied that cedants have taken appropriate measures? The answer lies in a dynamic update to trigger pre-requisites for subsequent bond tranches.

PRODUCT DESIGN: EVENT ONSET TRIGGER PRE-REQUISITES UPDATE

(a) Affected country introduces following measures:

- Curbing non-essential travel (to minimize spread risk) intra-country and overseas.

- Public announcement of the situation; usage of facial masks in public spaces and law enforcement against crowded gatherings (reference the Tablighi gathering in India) [c]

(b) Adjacent countries introduce the following measures:

- Track & trace foreign nationals and citizens with recent visits to the affected country.

- If required, quarantine should be imposed.

Again, the role of technology is important here to implement tracking (preferably via phone numbers). This would require PPP since inbound travellers might be requested to disclose their contact information in immigration forms which can be shared by Immigration authorities with the tracking software providers.

Hopefully, you’re now convinced as to why it is important for the ultimate cedant of risk (i.e. a Federal Government) to participate quota-share in premium payment.

Trigger event(s) definition

Given the above risk management functions embedded into the trigger pre-requisites, you might expect the trigger to be equally “complex”, thankfully not!

The trigger condition for the 1st tranche pay-out from the World Bank’s Pandemic Emergency Financing was: [iv]

(a) 250 deaths in the primary country

(b) A further 20 deaths in another country

Clearly, there is a design flaw here; recall the earlier observations that:

(i) Early response to pandemics imposes a positive externality on neighbouring countries; clearly, this bond only triggered after the pandemic has spread!

(ii) The Present Value of funding far exceeds future value in pandemics

Replacing the dual country breach trigger to a single country breach trigger at 100 deaths would save 4 days in context of the Covid-19 situation in Italy and France. (reference the image below extracted from the ECDC data on 05/04 [iii])

You’d be correct in stating that this could “downgrade” the bonds rating to near junk status. However, you could require investors in more secure tranches to purchase a pro-rata share in the junk tranche or provide tax relief via an CSR (Corporate Social Responsibility) note.

PRODUCT DESIGN: DYNAMIC TRIGGER EVENT DEFINITION

Single country with 100 death cases reported by a competent authority.

-> Tranche A pay-out triggered

-> Tranche B+ trigger pre-requisites modified as highlighted earlier.

20 death cases in secondary country reported by a competent authority.

-> Tranche B pay-out triggered

Subsequent tranches can follow a similar structure

The National Academy of Science recommends that “if there were a structure to allow money to come ahead of the risk onset, that would be interesting” [i]

That is what brings us to the next section – risk transfer and management via insurance instruments is only part of an overall solution, we need to look to the bond market.

Beyond insurance; Infrastructure matters

Especially for Low Income Countries, stockpiling resources for pandemic events and investing in public healthcare might be a far shot in the dark. This is where capital markets interact with insurance.

Investors in the parametric insurance instrument above have every incentive to reduce the spark and spread risk of a pandemic. Based on the WHO’s Pandemic Emergency Financing investors [iv], it seems (re)insurance entities and Pension Funds are the most likely investors.

Given their risk appetite and desire to diversify asset risk, a portfolio containing a parametric pandemic insurance product should contain a pandemic resilience infrastructure bond.

For those of you concerned around how low-income countries would be able to meet the trigger pre-requisites, the pandemic resilience bond is the answer:

(a) The beneficiary (low-income country) would benefit from a lower interest rate due to the credit rating of institutions providing long-term pledges. [17]

(b) Having the beneficiary bear part of the interest burden creates “skin-in-the-game” to judiciously spend funds.

(c) Investors in the parametric product would benefit from risk mitigation.

(d) Similar to Green Bonds, issuance could align with focus on ESG investing [18] and increased emphasis on CSR by corporates.

It goes without saying that you could use Open Banking (UK) or Account Aggregation (AA) equivalent frameworks to trace the expenditure of funds to minimize leakages.

Thus far, we’ve discussed a framework for product design:

In the next section, we will explore a specific product i.e. non-physical damage Business Interruption.

Go-To-Market

“No single, optimal response to a public health emergency exists; strategies must be tailored to the local context & to the severity and type of pandemic.”- NCBI [v]

In this section, I will highlight two separate geographies of interest.

United Kingdom

Nick Lamparelli, Chief Underwriting Officer at ReThought Insurance [19], highlighted that private (non-physical damage) business interruption product(s) would be a good starting point. The USA and UK are similar insurance markets in terms of maturity and propensity to purchase insurance.

For the UK, I would recommend a non-physical damage business interruption product which is serviced parametrically:

i. Open Banking framework: A collection of UK FinTechs formed ‘Covid Credit’ [20] to help UK SMEs access short-term relief from the UK Government.

ii. Add-on to existing business interruption products:

a. The BIBA (British Insurance Brokers Association) seems to be facing the brunt of BI claims denial (only 5% don’t have a pandemic exclusion) [21]

b. Given commercial insurance is primarily broker-intermediated and business owners are disappointed, there might be an opportunity here.

iii. Benefit structure tied to:

a. (Fixed and variable) wages

b. Fixed cost i.e. rent

By using body corporates and SMEs as the conduit for “pandemic aid”, the UK Government would be able to hit three birds with one stone:

- Delay furlough of all staff

- Help SMEs stay afloat

- Prevent property and lending markets collapse (some % of staff and SMEs will continue to be able to honour loan/mortgage obligations)

A “reimbursement” structure for pay-outs can be used via Open Banking to track funds disbursal.

India

Unlike the UK, India faces an inherent protection gap; pegged by Swiss Re at over 90% [22] i.e. in the event that an average Indian family’s main breadwinner passes away, their family has the ability to meet less than 10% of their projected future spending via insurance and savings.

For India, I remain sceptical as to whether SMEs would (even with Government) support be in a position to pay premiums for such insurance products. However, I see a clear path for individual protection and funds disbursal.

Open questions

Below are a set of questions which I don’t have an answer for:

i. How do you decide on a fair coupon on the pandemic resilience infrastructure bond?

ii. How will pandemic risk pricing be impacted in a post Covid-19 world? Is it still feasible?

iii. What tranche-based system works best? And, how can we get investors to purchase these instruments?

iv. How do we construct this facility to be multi-year?

I invite your constructive criticism, feedback and recommendations for change. If you’re keen to speak with me, please feel free to ping me at rahul@backstopinurance.uk

I believe there is a clear opportunity for private technology start-ups i.e InsurTechs to provide the platform, analytics and oversight to allow alternative capital to access pandemic risk and hedge against it appropriately via infrastructure bonds.

Disclaimer

Views expressed in this article are my own and do not reflect those of any associated entity.

This article does not constitute investment or any other form advice. The author bears no responsibility in the event of financial or other loss arising from actions taken by the reader or any related party on the basis of information represented in this article. The author does not have any financial interest in any firm mentioned in the article above; this article is produced for educational purposes.

Oh Rahul. I do not hv words to express my appreciation on this deep researched & thought provoking output. Each line in this article has something more to explore / learn.

This is such a wealth of information and food for thought!!