Update on InsurTech in India (Q2 FY 21)

Update on InsurTech in India (Q2 FY 21)

$185.6M in venture funding, regulatory progress and much more this quarter in India!

Hey folks! This post is my quarterly round-up of InsurTech activity in India; the Q1 edition was very well received and previous editions on LinkedIn have received 30K+ views!

Fundraising

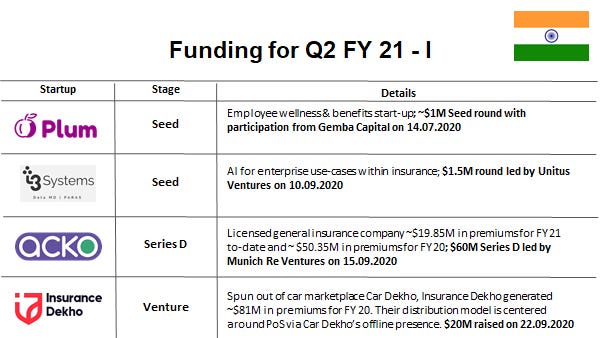

With $135.6M in primary capital entering the ecosystem, this quarter has been rather active on the ‘late’ stage.

PlumHQ and i3Systems raised their respective Seed rounds.

Acko’s $60M Series D funding has been doing the rounds for a while - so much that I wrote a piece titled ‘Blitzscaling Insurance with Acko’ in June. I’ve commented on the ~$400M to $500M valuation & their FY 21 progress a bit later in this piece.

InsuranceDekho - CarDekho’s insurance venture received $20M from its parent company.

Interestingly, Chinese insurance giant Ping AN led CarDekho’s $70M Series D in 12.2019 [1]

Perhaps, there is some ‘knowledge transfer’ here given Ping An’s investment in AutoHome (Chinese equivalent for CarDekho)?

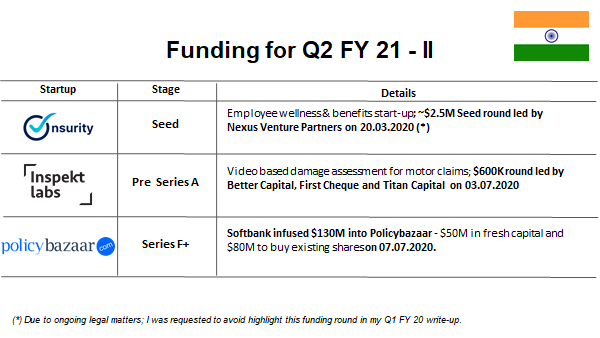

Techstars London alumni Inspekt Labs raised a $600K Pre-Series A.

Policybazaar ‘raised’ $130M ($50M primary infusion & $80M secondaries purchase) from Softbank. Rumour has it that Google is looking to infuse capital into Policybazaar at a $1.5bn valuation. [2]

I find it fascinating that Policybazaar’s valuation in private markets today is $1.5bn; however, it is looking at a NASDAQ IPO valuing the company at $3.5bn in ~12 months! [3] And, it looks to raise another $250M at a $2bn valuation.

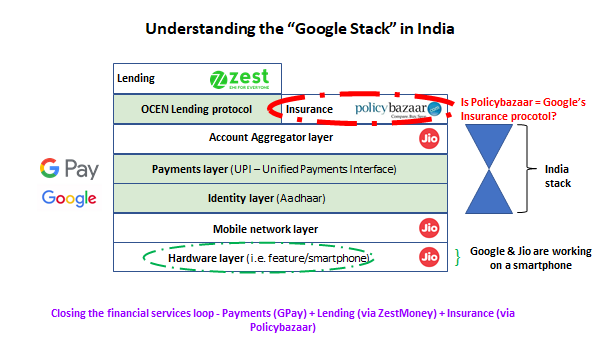

Putting my strategy hat on, Google x Policybazaar seems to be a perfect fit. The graphic below summarizes my thesis; Policybazaar could act as ‘Google’s insurance protocol’ in the Indian market.

My extended piece on Google x Policybazaar may be found here.

Switching gears from fundraising, let’s take a look at how regulation is ‘giving flight’ to InsurTech in India (in some cases, e.g. drone insurance, quite literally so).

Regulation as an enabler

If you’re not keen to delve into the regulations, feel free to scroll past the next 2 images where you’ll find a summary!

PS - Applications for cohort II of IRDAI’s InsurTech sandbox are open! [4]

Summary of key regulations

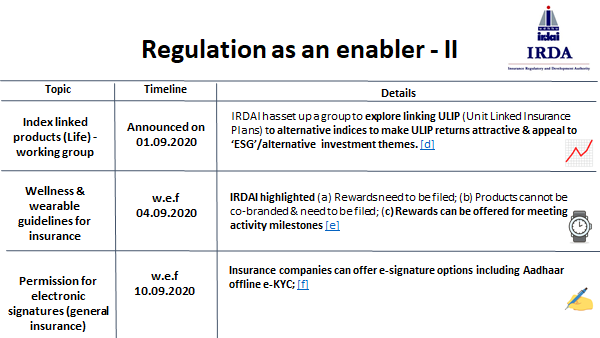

Digital signatures are acceptable for ‘risk-only’ (i.e. non-savings) life insurance products until 31.12.2020; this is perfect for ‘sachet’ term life products sold on ‘Bharat’s digital platforms’ e.g. Khatabook, Pagarbook and BharatPe (insurance experts may point out the “group” structure already sidestepped this - yes, you’re right too!)

KYC (Know Your Customer) can be done via video and via Aadhaar offline e-KYC for general (i.e. non-life) insurance; anything that brings the ‘expense ratio’ down in insurance (i.e. online KYC) is welcome!

Guidelines on wellness benefits in insurance [5]

Wearable-linked insurance products must cannot be co-branded with Technology partners :(

Activity points can be redeemed for rewards and premiums discounts upon renewals :)

The wearable guidelines set the tone for exciting ‘payer + provider health ecosystem’ plays - more so in light of iSPRT’s National Health Stack initiatives such as the ‘gamifier health policy’

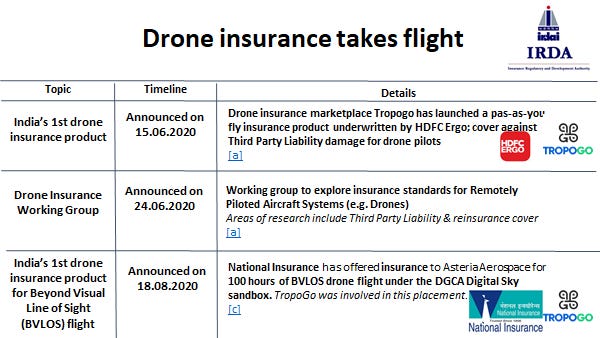

The above graphic explains how regulation is helping innovation take flight - it is exciting to see drone insurance take off in India; Digital Sky may just become a reality.

We’re about half way through - short break! If you have found this write-up useful so far, please do consider subscribing (if you haven’t already) -

Neo-insurer performance

Acko and Digit commenced operations at roughly the same point - as they come to their 3rd year anniversary, I felt a small section on their performance does justice to their respective growth.

Digit - all guns blazing

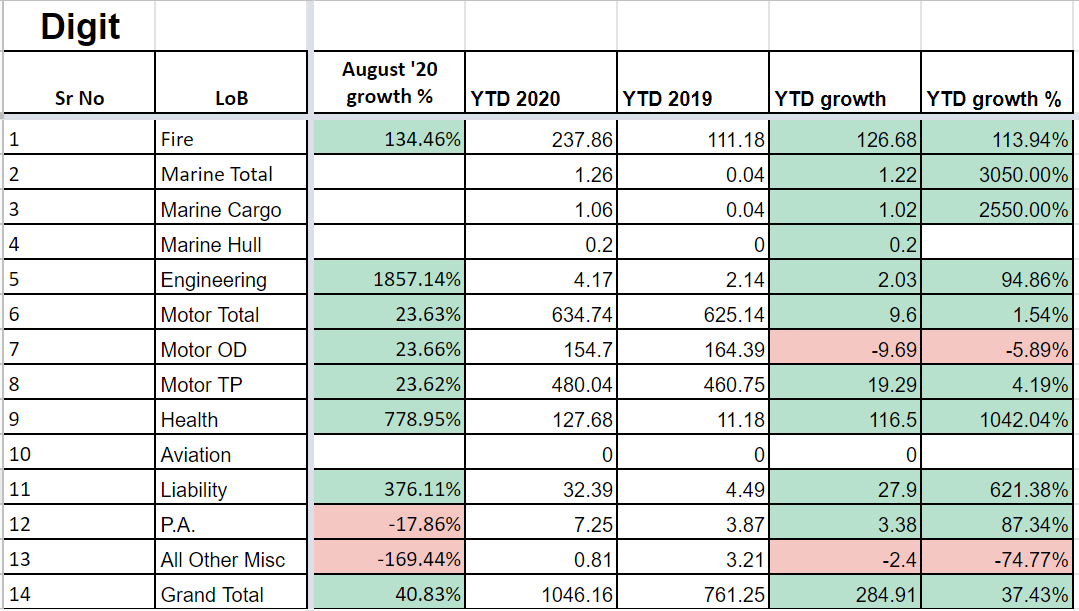

Fairfax backed Digit Insurance has written $141M (₹1046 crore) in premiums for FY 21 YTD (i.e. ~ 4 months). In FY 20, Digit wrote $296.73M in premiums; my FY 21 estimate for Digit’s premium sits between $400M and $425M.

Data from regulatory filings suggests:

Fire and Health insurance are major growth drivers

Digit has been working on its commercial insurance book (evident from the growth in its Fire and Liability business)

Digit’s emphasis on Group health insurance products and its Covid-19 insurance serve as the explanation for growth in its health business.

Diversification away from Motor

Positive news from an investor lens - Digit is increasingly becoming less reliant on motor insurance which powered its early growth (now evident from flattening figures).

Digit’s projections are astounding for a company that began trading in September 2017 - exactly 3 years ago! Their experienced ex-Allianz management team has a strong mandate - raising $84M at a $870M valuation in January; this would imply a forward premium multiple of ~2x - which is hardly generous given its growth potential.

Acko - pandemic struck?

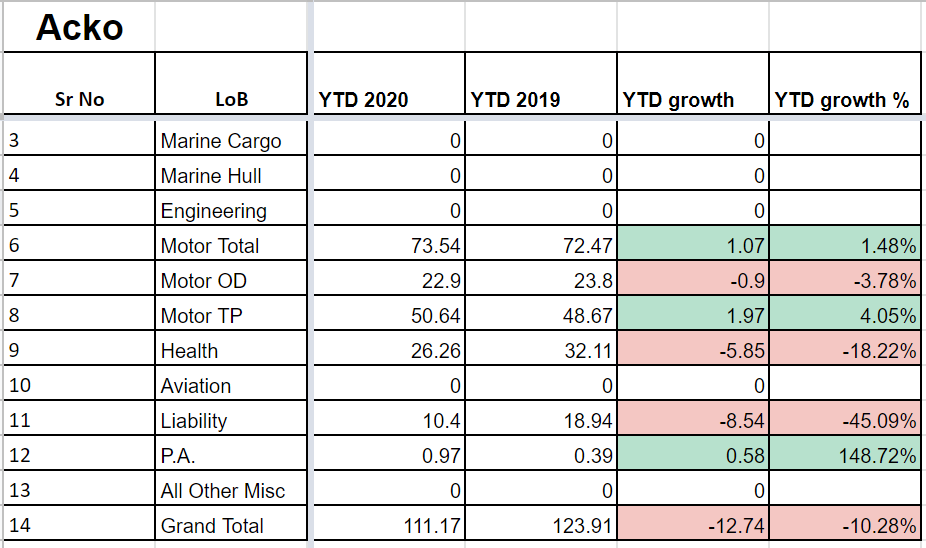

Acko’s recent raise values the company at ~$400M to $500M in this recent funding round. Acko has written $14.98M (₹111.17 crore) in premiums for FY 21 YTD (i.e. ~ 4 months). In FY 20, Acko wrote $50.41M in premiums; I am hesitant to provide a FY 21 estimate for Acko’s premiums since their business has dipped 10.2% due to Covid-19.

Data from regulatory filings suggests that Acko’s health insurance business has taken a hit. This come across as a surprise to me given how the health insurance segment has grown YoY on account of Covid-19

Assuming Acko is able to deliver $50.41M in premiums for FY 21 (its FY 20 figure) - Acko would be valued at a forward premium multiple of 10x - nearly 5 times that of Digit!

It would be unfair to compare both companies quite literally given Digit’s focus is on offline, commercial and broker sourced business whereas Acko’s focus is on ‘pure’ digital and digital partner driven business. But, this comparison was a helpful exercise for me.

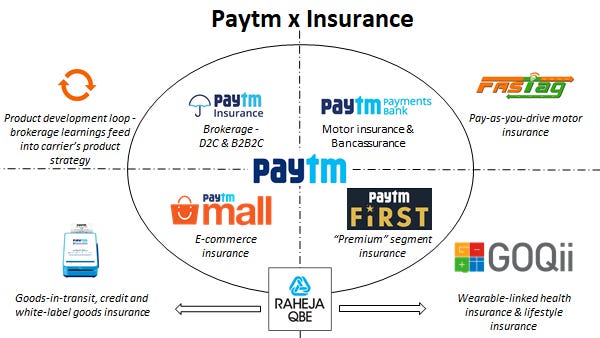

Bonus: Paytm & Insurance

On 07.07.2020, Paytm to announced its move to acquire Raheja QBE Insurance for ₹568 crore (i.e. $76.1M) [6] This move certainly baffled me - they acquired their insurance brokerage licence in March this year!

I have written about ‘Paytm & Insurance’ at length here

I’ve always marveled at consumer FinTechs treating ‘insurance as a feature, not a product’ by foraying into insurance distribution. However, could buying an insurance company become the ‘next frontier’? (Navi did so with DHFL Insurance)

That’s all for the Q2 FY 21 review - I look forward to your thoughts, comments and constructive criticism. Before you leave, I’ve got some small updates for you!

*Personal update* - I will be moving back to India to build a venture-backed InsurTech start-up. If you’re based in India and have bought an insurance policy in the last ~18 months, I’d love to chat with you @Rahul_J_Mathur

Update since publishing

The startup I co-founded — BimaPe — is now out of stealth mode. you can read a bit about what we are doing below.

Please note: Any views expressed above are my own and do not reflect those of BimaPe Inc, our investors, employers or customers.

About BimaPe

🏗️We’re building a consumer friendly digital insurance producton the India Stack (Account Aggregator, National Health Stack and UPI 2.0).

🧐You can discover hidden insurance benefits on your card here (no card number required) with BimaPe; join 4,500+ BimaPe members today!

📝You can subscribe to our daily Insurance Snapshots on WhatsApp here; join 1,800+ subscribers!

👶x5 open roles here.

‘Know Your Card’ by BimaPe is a tool for YOU to discover hidden insurance benefits on your card.